Health & Fitness

How Do We Pay For College Without Going Broke?

Information on maximizing your ability to get financial aid.

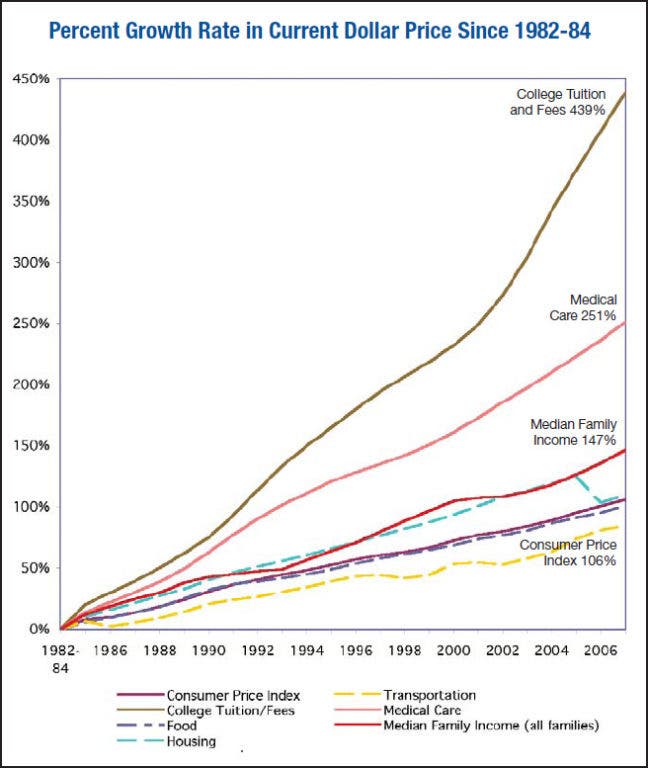

How do we pay for college when the rates are going up and up and our income is not? There are many ways to skin the tuition beast and peal off layers of the cost when the appropriate steps are made in college funding planning.

There are some of the fallacies that first need to be known:

- Financial aid is for people who have very little money.

- Parents with large incomes can’t qualify for financial aid.

- Private/expensive colleges are financially unattainable vs. the public/less expensive colleges.

- 529 plans are the best way to save money for your child for school.

- Scholarships can pay for the bulk of tuition.

- The financial aid package you receive is etched in stone and has no room for negotiation.

- Your entire net worth is used in determining your effective family contribution (E.F.C.).

These are the 7 points of light on those 7 fallacies:

Find out what's happening in Plymouthwith free, real-time updates from Patch.

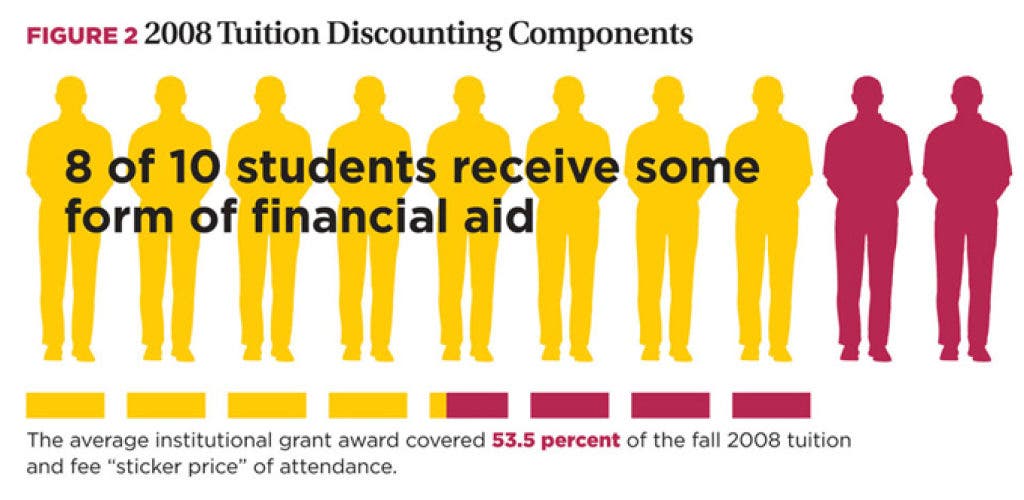

- Financial aid is awarded to all levels of income and all levels of net worth.

- Federal financial aid is based on the parent’s and the student’s income, assets, household size, the number of children in college and/or private school, as well as some other factors but there are no income level caps that limit a families eligibility.

- Every school’s aid formula is different and the amount of available aid is extremely different. For example Private School XYZ has a high tuition compared to Public State University in this case twice as expensive. Due to the large endowment and the percentage of need based aid given the net cost of the “expensive” private school ends up being less. The sticker price of a school is not what determines the net cost of that school.

- 529 plans are a great way to save money for your future college students but the approach and the ownership should be considered. The bottom line is reducing your E.F.C. and if the child owns the 529 the percentage of the asset is much higher than if the parents own the 529 and if the 529 is owned by the grandparents it is not considered an asset when determining the E.F.C.

- Unless you have an extremely talented athlete or a Rhode Scholar and are getting a “free ride”, scholarships make up about 3% of the overall tuition paid every year. The rest is paid by the Federal Government, the colleges and the families, either from their assets or through loans. That being said, there are a lot of great scholarships available and they should be researched, but the awards should not be counted on to pay for the net cost due to availability and amount.

- Often times award packages are sent to the home and the amount of the award is not up to the parent’s expectations and the desired school is not financially reachable based on the award package. Appeals are totally acceptable and there are many angles that can be used to write your appeal. For example, the federal government has changed some of the rules to determine income. Due to the high rate of layoffs and cutbacks people can use a 12 month future earnings estimate vs. the previous tax year earnings. Sometimes there are family unit changes, a death in the family, high medical or dependant care costs or a divorce. All of these and more are legitimate reasons for an appeal. Furthermore, this appeal can be done anytime during the student’s time at the college if a major change happens.

- The assets you hold are looked at based on a variety of factors. Simply put the typical family receives an asset protection allowance of $45,000 and 12% of the remainder is used to determine the E.F.C. Other less known facts, are that qualified retirement investment monies and life insurance policies are not considered part of your assets.

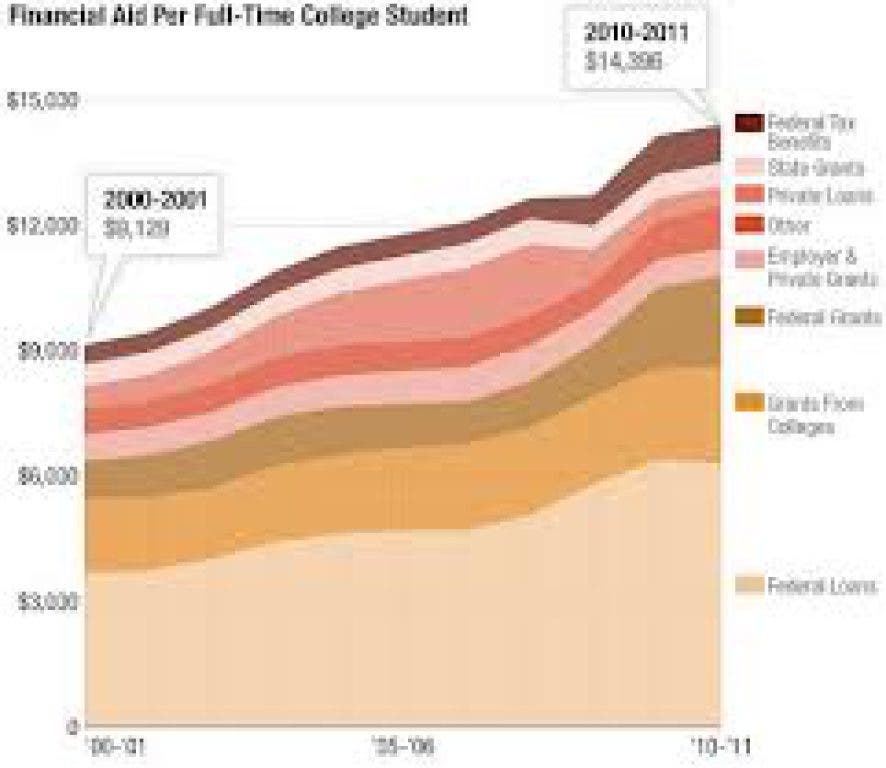

The bottom line is the cost of higher education is consistently going up, while our median household income is struggling to flat line. In order to offset this gap, families need to have a plan, start this plan as far in advance as possible and lower their E.F.C. in strategic/legal ways so as to qualify for more financial aid or “free money”. Furthermore, the children or future college undergrads need to buckle down the minute they enter high school and excel academically, athletically, personally and with extracurricular activities. It will take everyone involved in the process to be able to afford the school of your choice but it can be done.

In order to restructure your assets properly and legally to lower your E.F.C., you should consult your financial planner and/or a little unknown niche called college financial planners. College financial planners, can help you evaluate your financial situation and recommend appropriate ways to protect your assets and lower your E.F.C. After you pay for all your children’s tuition, the next big financial phase in your life is essentially retirement and parents need to keep that in the forefront of their mind.

Find out what's happening in Plymouthwith free, real-time updates from Patch.

New England Advisors Group, is a local group that has been working with families for many years and has enabled families to comfortably manage the tuition costs while helping them achieve their financial goals for retirement. New England Advisors Group is located at 175 Derby St. Suite #7 in Hingham. Their phone number is 781-740-1175.

All the information in this article is believed to be true and accurate. The statements in this article are for informational use only and should not be used to determine any financial planning without consulting a professional planner.